The insurance company creates and financially backs your policy, while the insurance agent is the licensed intermediary who helps you understand, buy, and manage it. These two roles are distinct, legally separate, and serve very different functions in the insurance lifecycle. Confusing them leads to wrong expectations during claims, coverage gaps, and frustration when something goes wrong. For Louisiana homeowners who have lived through hurricanes, floods, and the claims process that follows, understanding the role of insurance agent vs. company is not a technicality. It is the difference between knowing who to call and feeling lost when it matters most.

What is the role of insurance agent vs. company?

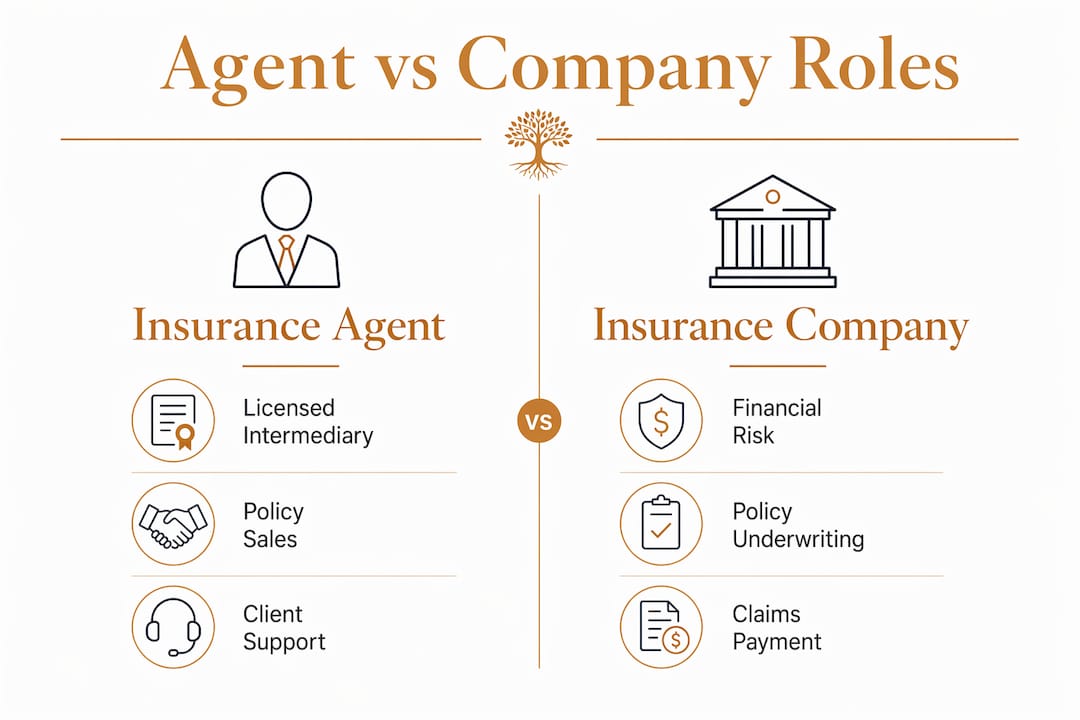

The clearest way to separate these two roles is by asking who carries the financial risk. Insurance carriers hold that risk. They design policy forms, set underwriting guidelines, collect premiums, and pay claims. The agent, by contrast, is a licensed intermediary appointed by the carrier to distribute those products and serve policyholders in the field.

In the industry, the formal term for the company side is the insurance carrier or insurer. The agent is sometimes called a producer. Both terms appear in state licensing records, appointment contracts, and policy documents. Knowing this vocabulary helps you read your own policy with more confidence.

What responsibilities does an insurance company carry?

Insurance carriers are the financial backbone of the entire system. Carriers underwrite risk, issue policies, collect premiums, and handle claims, while agencies and brokers distribute products. This means every dollar paid out after a hurricane, flood, or car accident comes from the carrier's reserves, not the agent's pocket.

Here is what carriers are specifically responsible for:

- Policy design: Carriers write the actual policy language, define covered perils, and set exclusions. An agent cannot change policy language.

- Underwriting and pricing: Carriers decide who qualifies for coverage and at what premium based on risk factors like location, claims history, and property condition.

- Claims payment: Carriers employ claims adjusters, review documentation, and issue payment decisions. Claims adjusters and carriers hold final financial decision-making power.

- Regulatory compliance: Carriers must meet state solvency requirements, maintain capital reserves, and submit to market conduct examinations. Missing claims deadlines can lead to fines and bad-faith litigation against carriers.

- Agent oversight: Carriers are responsible for agent appointments and licensing oversight, ensuring agents are authorized to sell specific products. State Departments of Insurance track these appointments closely.

| Carrier function | What it means for you |

|---|---|

| Underwriting | Your eligibility and premium are set by the carrier, not your agent |

| Claims authority | Only the carrier can approve or deny a claim payment |

| Policy language | Coverage terms are fixed by the carrier and cannot be altered by an agent |

| Solvency requirements | Carriers must maintain reserves so they can pay claims when disasters hit |

| Agent appointments | Carriers authorize which agents can legally sell their products |

Pro Tip: You can verify your agent's appointment and licensing status through the Louisiana Department of Insurance's online lookup tool. If an agent is not properly appointed by the carrier, any policy they sell may be invalid.

What are the key duties and limitations of insurance agents?

An insurance agent's primary job is to serve as the bridge between the carrier's products and your specific coverage needs. Agents act as licensed intermediaries legally representing insurance companies, while carriers hold financial risk and design policies. That legal representation matters. The agent works on behalf of the carrier, not as an independent advisor with fiduciary duty to you.

Here is what agents are authorized and expected to do:

- Assess your coverage needs: A good agent asks about your home's replacement cost, your vehicles, your flood zone, and your life situation before recommending coverage levels.

- Explain policy language: Agents translate carrier policy forms into plain language so you understand what is and is not covered before you sign.

- Submit applications: Agents gather your information and submit it to the carrier for underwriting review and approval.

- Manage ongoing policies: Agents process endorsements, coverage changes, and renewals on your behalf.

- Support claims documentation: Agents help you organize documentation and communicate with the carrier, but they cannot override a claims decision.

Agents also have real limitations that every policyholder should understand. Agents cannot bind coverage unless expressly authorized by their appointment contracts, and they are limited in making pricing or underwriting changes. If an agent tells you a price or coverage detail without confirming it with the carrier, that information may not be binding.

Insurance agents owe legal loyalty to the insurer, not the policyholder. This contrasts with insurance brokers, who owe a fiduciary duty to their clients. Agents must handle applications properly, honestly explain coverage, and forward premiums to insurers. But they are not legally required to find you the best possible deal across all carriers the way a broker would be.

Most states require agents to complete continuing education to maintain their licenses. Requirements vary widely. Massachusetts requires 45 hours every 3 years, while Kansas requires 12 hours every 2 years. This ongoing education requirement exists because policy language, state regulations, and coverage options change regularly.

Pro Tip: When your agent quotes you a premium or confirms a coverage detail, ask them to confirm it in writing from the carrier. This protects you if there is ever a discrepancy between what you were told and what the policy actually says.

How do agents and companies collaborate during the insurance lifecycle?

The agent and carrier work together at every stage, but their roles never fully overlap. Understanding this collaboration helps you know exactly who to contact and what to expect at each step.

- Application stage: You provide information to your agent. The agent submits it to the carrier. The carrier underwrites the risk, sets the premium, and issues the policy. The agent cannot guarantee approval or pricing before the carrier reviews the application.

- Policy management: When you want to add a vehicle, update your home's coverage, or change a deductible, you contact your agent. The agent submits the change request to the carrier. The carrier approves or modifies the request based on underwriting guidelines.

- Claims filing: You report a loss to your agent or directly to the carrier. Agents support claims by ensuring documentation is complete and providing interpretive assistance, but they cannot override carrier claims decisions or payment authority. The carrier assigns an adjuster, reviews the claim, and issues a decision.

- Regulatory timelines: Carriers must process claims within state-mandated timeframes. In Louisiana, carriers are required to acknowledge claims within a set number of business days and reach coverage decisions within 30 to 45 days. These timelines are the carrier's legal obligation, not the agent's.

Knowing who controls each step of the process removes the frustration of feeling like your agent is not doing enough. Your agent advocates for you and keeps the process moving. The carrier makes the financial decisions. Both roles matter, and the best outcomes happen when you work with an agent who knows how to communicate effectively with the carrier on your behalf.

Understanding this separation of roles reduces confusion during claims and policy interactions, enhancing consumer satisfaction. Louisiana homeowners who have filed claims after major storms know firsthand how important it is to have an agent who stays in contact, follows up with the carrier, and explains every step of the process.

How does knowing these roles benefit Louisiana homeowners?

Louisiana sits in the bullseye for hurricanes, flooding, and severe weather. That reality makes the agent vs. company distinction more than academic. It shapes how you prepare, how you communicate, and how quickly you recover after a loss.

Here is how this knowledge works in your favor:

- You know who to call first. For coverage questions, policy changes, and general guidance, call your agent. For claims status, payment disputes, or policy document requests, you may need to contact the carrier directly.

- You set realistic expectations. Your agent cannot speed up a carrier's claims decision or override an underwriting denial. Knowing this prevents misdirected frustration and helps you focus your energy on the right conversation.

- You avoid the fiduciary misconception. Many homeowners assume their agent is legally obligated to find them the best possible coverage at the lowest price. Agents owe a duty to act professionally and honestly, but they do not have a fiduciary duty to policyholders the way brokers do. Choosing an agent with a strong local reputation and a track record of honest advice matters more than assuming legal protection that does not exist.

- You choose agents with real authority and local knowledge. An exclusive agent appointed by a major carrier like Allstate has deep product knowledge and a direct line to carrier resources. That appointment relationship means faster communication and more reliable answers than working with an agent who has loose ties to multiple carriers.

Louisiana homeowners who understand these distinct roles navigate policy questions, claims, and coverage choices with far more confidence. Local expertise and peace of mind during storms outweigh saving small premiums elsewhere. That is not an opinion. It is what experienced policyholders consistently report after going through a major loss.

Key takeaways

The insurance company assumes all financial risk and controls policy terms, claims decisions, and underwriting, while the agent serves as your licensed guide through the entire process.

| Point | Details |

|---|---|

| Carrier holds financial risk | Only the insurance company can approve claims, set premiums, and issue policy language. |

| Agent is a licensed intermediary | Agents represent the carrier legally and help you understand and manage your coverage. |

| Legal loyalty runs to the insurer | Agents owe professional honesty to clients but do not have fiduciary duty the way brokers do. |

| Collaboration drives outcomes | The best results come from agents who communicate effectively with carriers on your behalf. |

| Local expertise has real value | A trusted local agent with carrier appointments provides faster answers and better advocacy after a loss. |

Why the agent you choose matters more than most people realize

After more than 20 years working with Louisiana families, I have seen the same scenario repeat itself. A homeowner buys a policy online or through an agent they barely know, pays the premium, and assumes everything is fine. Then a storm hits. The claim gets complicated. The homeowner calls the carrier and gets a call center. They call the agent and get voicemail. Nobody explains what the adjuster's report actually means. Nobody follows up.

The insurance company's job is to manage risk at scale. That is not a criticism. It is just the reality of how carriers operate. They process thousands of claims at once. Your individual situation is one file among many. The agent's job is to make sure your file gets the attention it deserves, that your documentation is complete, and that you understand every step of the process.

What I have learned is that the agent relationship is where the real value lives. A carrier can have excellent policy forms and strong financial ratings. But if your agent does not know your property, does not understand Louisiana flood zones, and does not pick up the phone after a hurricane, those policy forms do not help you much. The agent who knows your name, knows your coverage, and shows up in person after a loss is worth more than any premium discount.

The Root Agency deploys a mobile catastrophe response unit directly into disaster zones after major storms. That is not something a carrier's call center does. It is what a local agent with 20 years of Louisiana experience and a genuine commitment to the community does. Choose your agent the way you choose your contractor. Reputation, track record, and the willingness to show up when things go wrong.

— David

How The Root Agency serves Louisiana homeowners

The Root Agency is an Allstate exclusive agency based in Baton Rouge, serving all of Louisiana and Mississippi. Steve Root has operated the agency for more than 20 years, building on a 40-year family legacy in Louisiana insurance. The agency holds 356 Google reviews at 4.9 stars and was named to The Advocate's 2025 Best of Baton Rouge.

Whether you need home insurance coverage, flood protection, auto, life, or commercial coverage, the team at The Root Agency provides thorough education, honest guidance, and responsive service backed by a carrier with the financial strength to pay claims. Explore the full range of coverage options or call us at (225) 926-0160 to speak with an agent who knows Louisiana and will be there when you need them most.