Commercial auto fleet insurance is a single policy that covers multiple business vehicles under one agreement, replacing the need to manage separate policies for every truck, van, or car in your operation. For business owners and fleet managers in Louisiana and Mississippi, this commercial auto fleet insurance guide covers everything from mandatory coverage types to cost-reduction strategies built around the realities of operating in these two states. Whether you run five delivery vans in Baton Rouge or a 50-truck operation out of Jackson, the fundamentals of how to insure a fleet apply directly to your bottom line and your legal standing.

What does commercial auto fleet insurance cover?

Commercial fleet insurance, the industry's standard term for this product, bundles liability, physical damage, and specialty protections into one policy. Understanding each component prevents the coverage gaps that cost businesses thousands of dollars when a claim is denied.

Liability coverage pays for bodily injury and property damage your drivers cause to others. This is the non-negotiable foundation of any fleet policy in Louisiana and Mississippi, and state minimums are just the starting point for most commercial operations.

Physical damage coverage splits into two parts:

- Collision covers damage to your vehicle from an accident, regardless of fault.

- Comprehensive covers theft, weather events, vandalism, and other non-collision losses. Note that physical damage coverage is not federally mandated, but lenders and equipment lessors almost always require it for financed vehicles.

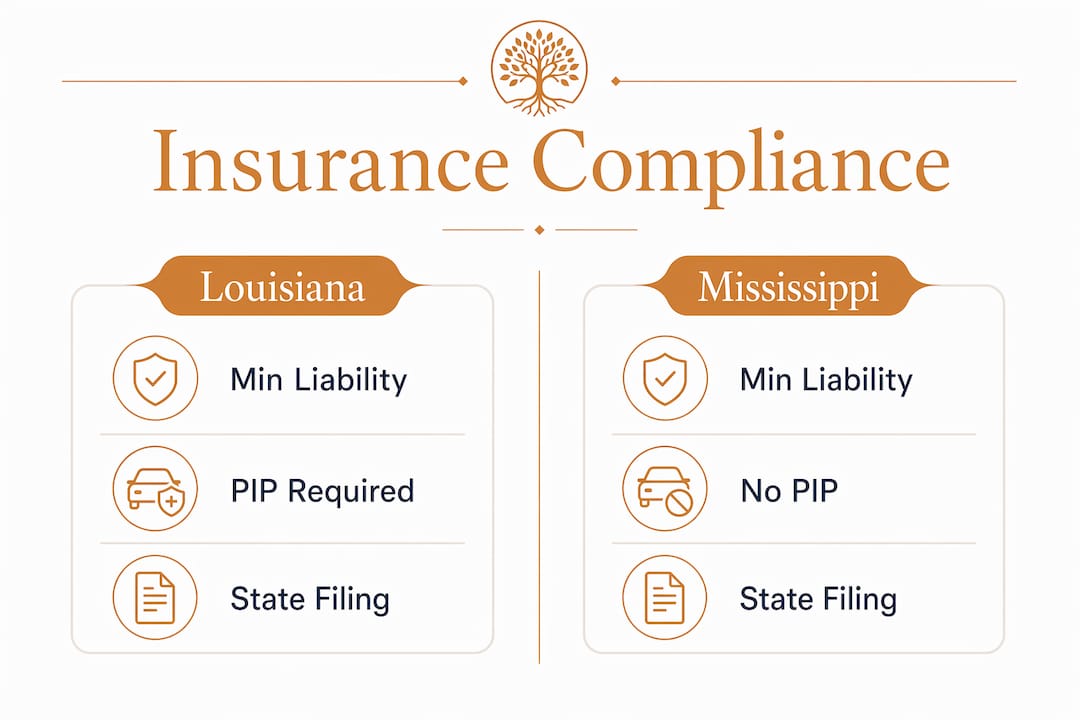

Medical payments and PIP cover injuries to your drivers and passengers. Louisiana requires Personal Injury Protection as part of its no-fault framework, while Mississippi operates under a tort system. Your policy structure must reflect which state your vehicles are primarily registered and operated in.

Cargo and goods-in-transit coverage protects the freight your vehicles carry. This is separate from vehicle liability and is critical for any fleet hauling client property or retail goods.

Hired and non-owned vehicle coverageextends protection to vehicles your employees rent or use personally for business purposes. Many fleet managers overlook this until a claim surfaces involving a rental truck or an employee's personal car used for a delivery.

Pro Tip: Ask your agent to confirm that hired and non-owned coverage is explicitly listed as an endorsement on your policy, not just assumed. It is one of the most commonly missing protections on fleet policies.

How to comply with federal and state insurance requirements

Federal and state compliance is not optional, and the penalties for getting it wrong are severe. Carriers operating under FMCSA authority face daily civil penalties up to $16,000 and immediate out-of-service orders for insurance lapses. That means your trucks sit idle and your revenue stops while the violation is resolved.

The FMCSA sets financial responsibility minimums under 49 CFR §387.9. Federal liability minimums range from $750,000 for general for-hire freight over 10,001 lbs GVWR, to $1,000,000 for non-bulk hazardous materials, to $5,000,000 for bulk hazardous materials. These are floors, not ceilings. Your actual exposure in a serious accident can far exceed these numbers, which is why most experienced fleet operators carry limits well above the federal baseline.

The BMC-91 filing is the FMCSA's proof-of-insurance form. Your insurer files it directly with the FMCSA, and continuous coverage with no grace period is required. If your policy lapses, your operating authority is suspended immediately. Your insurer must notify the FMCSA 30 days before cancellation, which gives you a window to act, but only if you are paying attention to renewal dates.

Louisiana and Mississippi both require minimum liability coverage for commercial vehicles registered in-state, with amounts that vary by vehicle class and use. Interstate carriers must align their state filings with FMCSA requirements, and insurance policies for interstate operations must carry endorsements beyond simply meeting minimum dollar limits.

| Requirement | Louisiana | Mississippi | Federal (FMCSA) |

|---|---|---|---|

| Minimum liability (general freight) | State commercial minimums apply | State commercial minimums apply | $750,000 |

| Hazardous materials (non-bulk) | Follows federal floor | Follows federal floor | $1,000,000 |

| Bulk hazardous materials | Follows federal floor | Follows federal floor | $5,000,000 |

| Continuous coverage required | Yes | Yes | Yes, no grace period |

Pro Tip: Set a calendar reminder 60 days before your fleet policy renewal date. That window gives you time to shop coverage, confirm BMC-91 filings are current, and avoid any lapse that would trigger FMCSA suspension.

How to choose the right fleet insurance policy for your business

Selecting the right policy starts with understanding your fleet profile: how many vehicles you operate, what class they fall into, what cargo you haul, and where your drivers operate. Each variable affects your premium and your coverage needs.

Named driver vs. any driver policies represent the first major decision. Named driver policies list specific operators and typically carry lower premiums because the insurer can price based on individual driving records. Any driver policies cover anyone operating a fleet vehicle with permission, which suits businesses with high driver turnover or shared vehicle pools.

Key factors that affect your premium include:

- Fleet size and vehicle class. Heavier vehicles carry higher liability exposure and cost more to insure.

- Driver history. A fleet with multiple drivers carrying moving violations or at-fault accidents will pay significantly more than a fleet with clean records.

- Annual mileage and operating radius. Local delivery fleets in New Orleans or Biloxi carry different risk profiles than long-haul carriers crossing state lines.

- Claims history. Insurers look at your loss runs, typically three to five years of claims data, before quoting.

When evaluating insurers, prioritize those with direct experience in Louisiana and Mississippi commercial markets. Insurance costs in Louisiana are among the highest in the nation due to litigation rates, weather exposure, and infrastructure factors. An insurer unfamiliar with this market may underprice your policy initially, then non-renew after the first major claim.

Review your Certificate of Insurance carefully before signing any contract. COI limits must meet contract minimums, and endorsements like Additional Insured and Waiver of Subrogation must actually appear on the policy before they can be listed on the COI. A mismatch between what the COI shows and what the policy contains causes contract rejections and can cost you a client relationship.

Pro Tip: Request a copy of the actual policy endorsements, not just the COI summary, before finalizing any fleet insurance contract. The COI alone does not confirm that required endorsements are in place.

Effective strategies to lower fleet insurance costs

Reducing your fleet insurance premiums requires a combination of technology, culture, and discipline. Here are the most effective approaches, ranked by impact:

- Deploy telematics and dashcams. Telematics systems monitor speed, braking, acceleration, and route data in real time. Sharing telematics data with your insurer can qualify your fleet for 10 to 25% usage-based discounts, and dashcams reduce collision rates significantly by creating accountability and providing evidence in disputed claims.

- Build a formal safety program. A clean fleet safety record qualifies fleets for performance-based discounts from most commercial insurers. Document your driver training, set written policies for phone use and hours of service, and conduct regular safety meetings. Insurers reward this with better rates at renewal.

- Conduct regular vehicle maintenance. A well-maintained fleet generates fewer mechanical-failure claims and demonstrates to insurers that you manage risk proactively. Keep maintenance logs for every vehicle and make them available during underwriting reviews.

- Adjust deductibles strategically. Higher deductibles lower premiums but increase your out-of-pocket cost per claim. The right balance depends on your fleet's claims frequency, your cash flow, and the strength of your safety program. A fleet with strong safety controls can often absorb a higher deductible without meaningful financial risk.

- Leverage claims-free discounts. Most commercial insurers offer renewal discounts for fleets that complete a policy period without a claim. Communicate your claims-free status to your agent at renewal and ask specifically what discount it qualifies you for.

Best practices for managing and updating your fleet policy

A fleet policy is not a set-it-and-forget-it document. Vehicles are added, drivers change, and contracts evolve. The most common administrative error that causes claims denial is a newly acquired vehicle that was never added to the policy schedule. Adding new vehicles within 30 days of acquisition prevents coverage gaps and keeps your schedule accurate.

Key management practices every fleet operator should follow:

- Notify your insurer immediately when adding or removing vehicles. Do not wait until renewal. Most policies have a grace period for new acquisitions, but it is short and not guaranteed.

- Reconcile your vehicle schedule at every renewal. Treat renewal as an accounting exercise. Compare your current vehicle list against the policy schedule line by line to catch vehicles that were added but never billed, or vehicles that were sold but are still generating premium.

- Verify COI accuracy before submitting to clients or partners. The COI alone is insufficient to confirm contract compliance. Confirm that every required endorsement is attached to the underlying policy before the COI is issued.

- Establish a workflow for rapid policy changes. Designate one person in your organization as the fleet insurance contact. That person owns the relationship with your agent and is responsible for communicating changes within 24 to 48 hours of any fleet modification.

- Monitor renewal dates across all policies. If your fleet insurance and your general liability renew on different dates, you risk a gap in coordinated coverage. Work with your agent to align renewal dates where possible.

The vehicle schedule reconciliation process at renewal also catches overcharges. Vehicles that were sold mid-term but left on the schedule generate premium you should not be paying. A thorough reconciliation typically saves fleet operators money while tightening their coverage.

Key takeaways

A well-structured fleet insurance policy, actively managed and aligned with FMCSA requirements, is the single most important risk management tool a commercial fleet operator in Louisiana or Mississippi can have.

| Point | Details |

|---|---|

| Coverage starts with liability | Bodily injury and property damage liability is the non-negotiable foundation of any fleet policy. |

| Federal minimums are floors | FMCSA minimums range from $750,000 to $5,000,000 depending on cargo type and vehicle class. |

| Telematics cuts costs | Sharing telematics data with your insurer can qualify your fleet for 10 to 25% usage-based discounts. |

| COI verification is critical | Always confirm required endorsements appear on the actual policy, not just on the COI summary. |

| Update schedules immediately | Adding new vehicles within 30 days prevents the most common cause of commercial fleet claims denial. |

What 20 years of fleet insurance conversations have taught me

After two decades of working with business owners across Louisiana and Mississippi, the pattern I see most often is this: fleet managers treat insurance as a compliance checkbox rather than a risk management tool. They buy the minimum, file the BMC-91, and move on. Then a serious accident happens, and they discover their limits were too low, a driver was not listed, or a vehicle was never added to the schedule.

The operators who sleep well at night do three things differently. They invest in telematics early, before an insurer requires it. They treat renewal as a financial audit, not a rubber stamp. And they build a real relationship with a local agent who knows Louisiana and Mississippi law, not just a national call center that processes their renewal automatically.

I also see fleet managers underestimate the deductible question. Raising your deductible to lower your premium makes sense if your safety program is strong and your cash flow can absorb a $5,000 or $10,000 out-of-pocket hit. It makes no sense if you are running a thin margin and one bad month could create a cash crisis. The right deductible is a business decision, not just an insurance decision.

The COI issue is the one that surprises people most. I have seen contracts fall apart because a client required an Additional Insured endorsement, the COI showed it, but the endorsement was never actually added to the policy. That is not a paperwork problem. That is a coverage problem. Verify the endorsements on the policy itself, every time.

— David

Get the right fleet coverage from a team that knows Louisiana and Mississippi

Running a fleet in Louisiana or Mississippi means dealing with some of the most demanding insurance conditions in the country. Weather exposure, litigation rates, and complex federal compliance requirements all add up. The Root Agency brings more than 20 years of hands-on commercial insurance experience to fleet operators across both states, with the local knowledge to match coverage to your actual risk.

Whether you operate five vehicles or fifty, our team builds fleet policies around your specific operation, not a generic template. We handle the compliance details, the COI verification, and the renewal reconciliation so you can focus on running your business. Explore your commercial fleet coverage options or call us at (225) 529-1990 to speak with someone who knows your market. You can also review our full range of business insurance products to see how fleet coverage fits into your broader risk management plan.